The Fifr Effect: How Fifr can buy you 5 years of financial freedom (without working more, spending less, or getting higher returns)

The uncomfortable truth: you’re likely making obvious money mistakes.

I’ve spoken with hundreds of young, high‑earners over the past few years. If you’re like most of them, you’re making avoidable mistakes that will cost you years of financial freedom.

What surprises me most? People will grind for years at a stressful job for a paycheck, but often won’t spend just one afternoon setting up systems that make their money work harder for them.

And why not?

- It’s uncomfortable (and boring). Facing past money mistakes isn’t fun. Scrolling through TikTok is way easier than looking at your budget.

- No instant feedback. There’s no immediate penalty for procrastinating your Roth IRA and no immediate windfall for actually doing it. Often good decisions can feel bad short‑term (e.g., you invest and markets dip).

- It’s confusing. The internet is noisy, and tax rules are complex.

So, we rationalize: “I’ll figure it out later. I’m doing fine. It’s not that big a deal if I figure out my financial plan later”

As a former investment banker, I built a model to test out that theory. With Fifr, a focused setup in one afternoon can put you on a path to move your financial freedom date forward ~5 years and make you millions of dollars richer. This is about cash management, automation and tax efficiency—not working more, not spending less, not even getting better investment returns.

You can check my work. I’m sharing the model so you can review the assumptions or use it as a basis for your own situation. Download the model »

Let me walk you through an example:

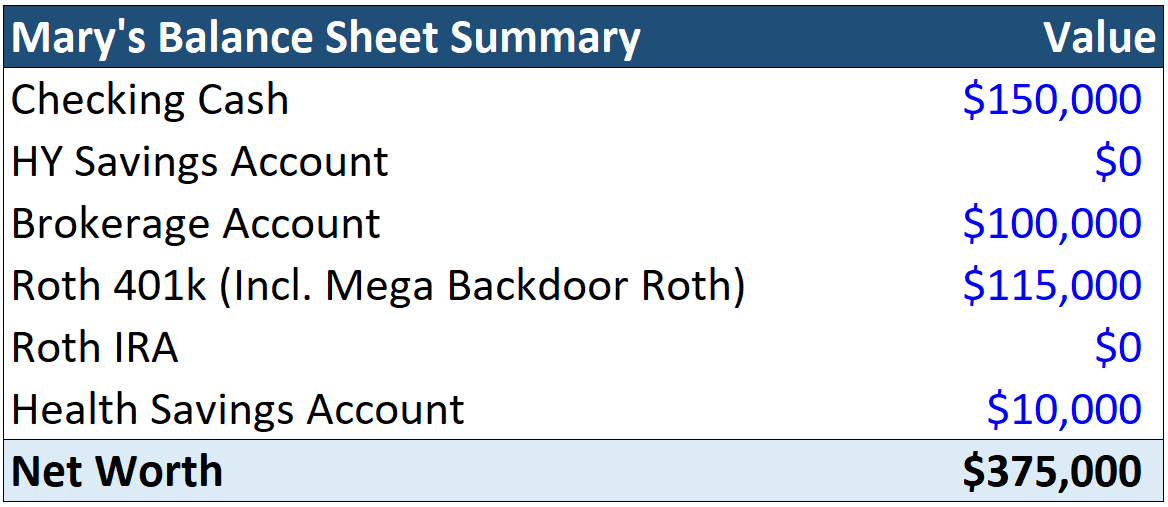

Meet Mary

- She’s 29 years old

- Lives in San Francisco

- Annual Income: $320,000

- Monthly Spend: $9,000

- Financial Goal: Leave her job to comfortably travel the world indefinitely with $16,000/month after tax

Her Balance Sheet is below

What Mary is already doing well

- Contributing $10k/yr to her 401(k) and investing it (contribution amount grows with inflation).

- Maxing out her HSA for tax benefits

- Investing half of her cash once per year during an annual review

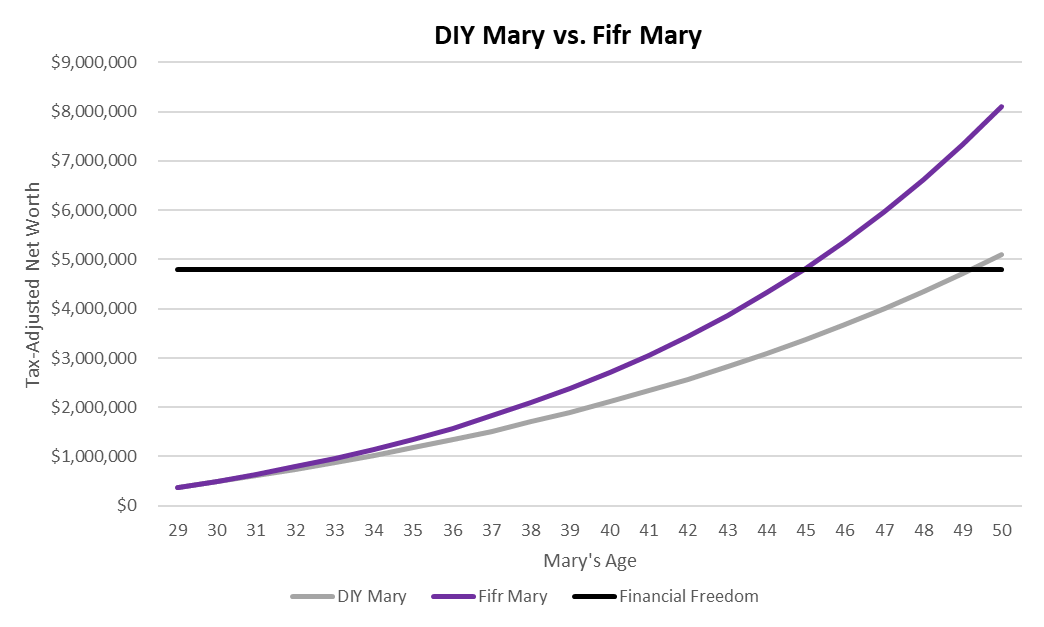

On this path, Mary is projected to reach her $4.8M tax‑adjusted net worth goal around age 50. That’s when she can realistically leave work and travel the world on $16k/month.

The Fifr Difference (same income, same lifestyle, same investment returns)

After onboarding, Fifr evaluates Mary’s position and automates the money moves she’s been missing:

- Employee Stock Purchase Plan (ESPP)

Fifr enrolls Mary into her ESPP plan at work, automates contributions, and sells shares ASAP after purchase to capture the built‑in spread. - Mega Backdoor Roth 401(k)

Since her plan supports after‑tax 401(k) contributions with in‑plan Roth conversions, Fifr helps Mary boost her 401(k) tax‑advantaged savings to $70k instead of $10k. - Backdoor Roth IRA

Fifr automates a Backdoor Roth IRA strategy that gives Mary the full tax advantages of a Roth IRA and gets around the income threshold. - Tax‑Loss Harvesting

Fifr implements automatic tax-loss harvesting, allowing Mary to claim an income tax deduction.

- HSA auto‑invest

Fifr spots the checkbox she missed and toggles auto‑invest so HSA contributions move out of cash and into investments. - Right‑sized emergency fund

Instead of parking ~50% of liquid assets in cash, Fifr sets 3 months of expenses (split: 1.5 in checking, 1.5 in HYSA) and invests the rest automatically in line with Mary’s needs. - Move from annual lump‑sum to automated monthly investing

Fifr automates monthly investing for Mary, saving her time and allowing for more time in the market.

None of these are theoretical. We’ve helped hundreds of members implement these optimizations and automations in real life.

Then Fifr keeps Mary optimized. For the purposes of this model, we kept Mary’s assumptions very clean and consistent. But in real life, things change. Raises, promotions, or new benefits may require adjustments. Major life events—buying a home, getting married, starting a family—can all reshape her financial picture. Add to that the annual reset of IRS contribution limits, and there’s always something new to account for. Fifr doesn’t just set and forget; we provide ongoing support so members can navigate these transitions and stay both in control and properly automated.

Projected Results: Mary with and without Fifr

- DIY Mary: Reaches $4.8M (tax‑adjusted) at age ~50.

- Fifr Mary: Reaches the same $4.8M at age ~45. That’s an extra 260 weeks of international adventures instead of being stuck at her office job. Yes, this is after factoring in Fifr’s flat fees.

- In fact, if she keeps working to 50, Fifr Mary is projected to end up near $8.1M (tax‑adjusted)— $3M+ more than DIY Mary—without changing income, spending or investment returns.

“Tax‑adjusted” = our estimate of after‑tax liquidation value, accounting for capital‑gains taxes under today’s rules.

Why this works

It’s the combination of prudent cash management, more tax‑advantaged contributions, and systematic investing—all enforced by proactive monitoring and automation so you can spend as little time as possible on your finances, while getting the most benefit.

- Cash Planning. Figure out how much cash you really need for your near-term goals, and invest the rest to let it grow for you.

- Tax shelters first. Max what the IRS lets you shield (401(k)+Mega, HSA, IRA)

- Automation beats Inspiration. Inspiration is energizing when you have it and disheartening when you don’t. Automation keeps you progressing even when the spark of inspiration isn't there

Why this can understate Fifr’s value

This model captures just a portion of what’s easy to quantify: tax advantages, automatic investing, and smarter cash management. It doesn’t fully capture the compounding from better real‑world decisions and having a team watch over your finances. Here are major sources of value we can’t cleanly model:

- Giving you visibility and control: We give you a dynamic picture of where you stand and where you need to be to hit your financial goals.

- Navigating life changes: Job updates, open enrollment, marriage, a new baby, or a home purchase all change your optimal moves. We’re with you to update your plan and automations so nothing falls through the cracks.

- Decision Support: Should I buy this house or keep renting? Refinance or not? Fund a 529? In several cases we’ve advised against moves we believe would have been expensive mistakes, and we helped others move forward on dream purchases with a clear plan.

Model assumptions & notes

- Inflation: 2.5%/yr for after‑tax income, expenses, cash needs and IRS limits.

- Tax rates: 22.5% long‑term capital gains rate; 46.65% marginal income rate (federal + CA assumptions).

- Tax-Loss Harvesting: $3,000 income tax deduction from tax-loss harvesting.

- Investment Returns: Nominal pre-tax investment returns of 8.5%.

- HYSA and Cash Returns: 4% pre-tax yield on HYSA and 0% yield in checking cash.

- Plan features: ESPP discount (15% of income at 15% discount) and Mega Backdoor availability.

- Risk: Investing involves risk, including loss. ESPP outcomes and market prices can vary at purchase/sale. Tax laws and plan rules change.

This article is for informational and illustrative purposes only and does not constitute legal advice, tax advice, investment advice or a recommendation to buy, hold or sell any security. The scenarios depicted above are hypothetical and are not based on actual people, investment decisions or returns. All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results. Financial planning and decision-making are highly dependent on the specific situation of the individual. Consult a qualified investment or accounting professional before implementing any of the financial strategies for yourself. Fifr may discuss or link to third-party content; such content is not endorsed and may not reflect our views. For important disclosures and our Form ADV, visit https://adviserinfo.sec.gov/firm/summary/328620.